In the last few days we have been reading in the local and international press about the collapse of Silicon Valley Bank, Signature Bank, the decline of Credit Suisse shares – as they reached an all-time low, ¼ of their value – together with the withdrawal of deposits, and other banking shocks which worries investors and depositors in both America and Europe. The first months of the new year have been marked by successive events that have shaken banking credibility, bringing back the bleak memories of 2008 with the collapse of Lehman Brothers.

Should depositors be worried? How close are we really to another global economic recession? Who’s to blame for the new crisis in the banking system? Are these isolated cases or other banks will fall in a downward spiral due to globalization, similar to Covid19 disease which spread from China to the rest of the world?

We must recognize that the US government moved quickly to protect the depositors of SVB and SB banks. Accordingly, the Central Bank of Switzerland took immediate measures supporting Credit Suisse with the necessary injection of liquidity, 50 billion euros, to restore confidence and prevent further sell-offs by its main investors. The news about Credit Suisse brought panic to the stock markets and the banking system in the whole of Europe, with shares falling in Societe General SA, BNP Paribas, Deutsche Bank, Barclays, and even in the Greek stock market.

Historically, since the founding of the first banking institutions in Europe and America, when deposits were at risk due to financial crises, customers ran to withdraw their money. Human psychology hasn’t changed much since then, if at all. Are we experiencing a repeat of the 2008 global financial crisis?

We are in a rather burdened macroeconomic environment where inflation dominates and analysts around the world are trying to explain and rationalize the persistence of rising prices. Geopolitical tensions, the energy crisis, the ongoing war in Ukraine, the pandemic, and other deteriorating factors fill the current picture. Signature Bank, for example, had significant exposure to the panic of the collapse in the value of cryptocurrency investments. Is there a common factor causing the current systemic crisis in banks regardless of their size or investment positions?

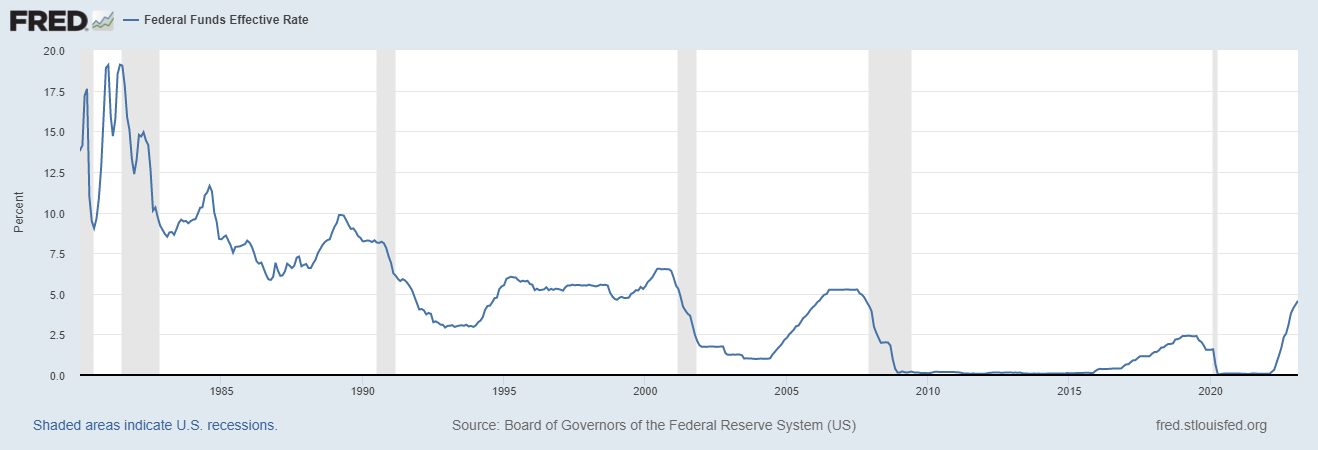

Let’s look at the chart below that illustrates the evolution of interest rates historically by the FED. One does not need to be a star in economics to understand that the continued increase in interest rates is one of the most important reasons that have brought about the crisis experienced by the aforementioned commercial & investment banks, the shocks in the markets, the imminent concerns of central banks and governments. The reason is simple in its complexity and the complexity of a globalized banking and financial environment.

High interest rates intended to reduce inflation – a constant loss of real income in citizens’ pockets and purchasing power – have the following negative effect on the banking sector. They effectively sell off the banks’ own long-term holdings and investments in government bonds since the banking institutions basically prefer to lend today cheaply (remember negative interest rates for a long time alongside QE, the monetary policy of quantitative easing) to enjoy significant returns from long-term government bonds which are directly affected as evidenced by the case of the banks that collapsed from the imposed increase in interest rates.

In the absence of today’s inflation, in the absence of the historically high inflation that the entire world is experiencing today, central banks would not need to raise interest rates to deal with it and prevent a recession that appears to be on the way if it hasn’t already started. The European Central Bank proceeded with a new increase in interest rates amid the panic caused by the systemic crisis at Credit Suisse and American banks. No one knows how the international market will react as long as high interest rates remain and the value of the banks’ long-term assets in bonds is gradually lost. That’s why the panic from Silicon Valley Bank and the connected technology sector including the crypto market, began to spread to the rest of the banks as long as the common denominator of interest rates remains at the levels they are. This is why the central banks in America and Switzerland moved very quickly with guarantees in order to restore banking confidence, to maintain liquidity, to bring back a desired normalization in share prices and by extension, the value of bonds.

Central banks and governments need to send the right messages through their economic policy. First of all put a limit on the increase in interest rates otherwise the panic, fear, lack of confidence and the loss of the value of the long term bonds, will bring new bankruptcies, massive withdrawal of deposits and investments, leading with mathematical precision to a new global recession.

Efstathios Kassios

https://stathiskassios.blogspot.com/

Original article in Greek published in Apopseis – Political Views: https://apopseis.gr/poso-konta-imaste-se-mia-nea-pagkosmia-yfesi/

-

How close are we to another global recession?

In the last few days we have been reading in the local and international press about the collapse of Silicon Valley Bank, Signature Bank, the decline of Credit Suisse shares – as they reached an all-time low, ¼ of their value – together with the withdrawal of deposits, and other banking shocks which worries investors… Continue reading

Leave a comment